What to Know: New Farm Lease Rules

Prepare for new accounting methods for your farm

In December, new accounting standards for reporting leases are scheduled to go into effect. The intention: To more accurately portray leases’ implications for a company’s financial health.

Under the new ASC 842 standards, companies must report both operating leases and finance (formerly called capital) leases on their balance sheets. Also, quarterly or monthly reports adjust balances of liability and “right to use” value.

“This will place a significant accounting burden on operations that use leases,” says Fallon Savage, senior vice president, agribusiness credit at Farm Credit Services of America. “Leases are not all entered into at the same time, nor do they end at the same time. Details of formerly ‘off balance sheet’ operating leases will need to be identified, pulled together and reported.”

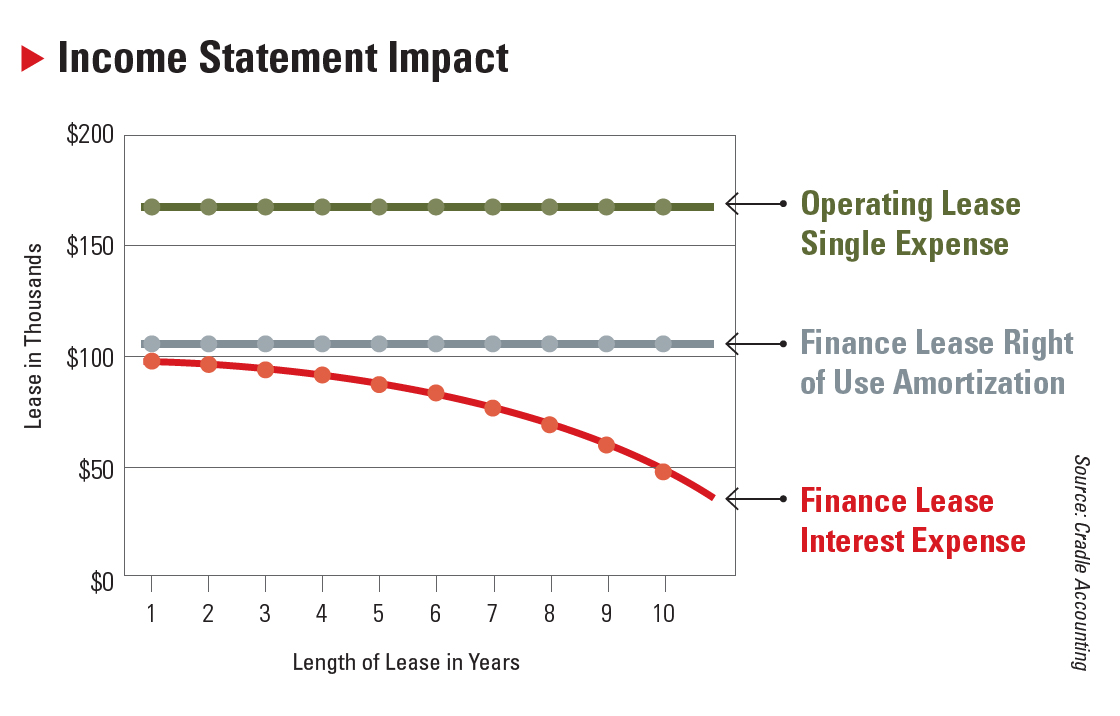

On the cash flow statement, short-term operating leases are treated as a single expense, but finance leases are reported as operating principal plus interest payments over the term of the lease.

The related amortization calculations will mean more work for accountants but likely not as much for most farmers, notes Paul Neiffer, CPA with CLA. Plus, accounting companies have had time to develop programs to spit out the values.

NOT ALL WILL BE AFFECTED

The new standards apply to operations following Generally Accepted Accounting Principles (GAAP) or Farm Financial Standards Council recommendations.

“I estimate some 20% to 30% of those who make their living from their agricultural operation will be affected,” Neiffer says.

The new reporting system shows “right of use values” for the asset under lease — but those assets are not treated as equity.

“As a result, leverage measures such as the debt:equity ratio will be affected,” Savage says.

This could push a farm over lending thresholds. Bankers could simply back the lease out, Neiffer says, or adjust their ratio thresholds.

“We are having conversations with some of our customers,” Savage says. “So far, we are looking at qualifications on a case-by-case basis and, when appropriate, we consider total liability less the lease liability.”

Discuss the new rules with your financial team to allow for the paperwork and time to go over the numbers with your lender.